| Latest | Greatest | Lobby | Journals | Search | Options | Help | Login |

|

|

|

This topic is archived. |

| Home » Discuss » Editorials & Other Articles |

|

| Demeter

|

Thu Nov-26-09 08:33 AM Original message |

| Weekend Economists Salute America's Turkeys November 26-29, 2009 |

|

Edited on Thu Nov-26-09 09:20 AM by Demeter

Yes, the markets are closed, which means WEE is open! In order to preserve my fingers, I'll just keep this posting running the whole 4 days. Unless it gets too long, in which case, look for a link to part 2....

Are you able to set your anxieties, paranoia and doubts aside for this special weekend? If you can, you are probably in the minority, but more power to you! You will be leaders with the energy to keep the Movement going. Are you cooking with your hands, while doing contingency planning in your head? Then you are the brainpower that will get us all through trying times. Are you feeling like pulling the covers over your head and waiting for another day? You aren't alone. Take comfort in your numbers, and know that when you are ready to take that first step, WEE will be with you, providing the best information and analysis available and providing a support group. So, before the turkey has to go into the oven, before rolling out the pie crust, have at it! Post what you have. And from all of us to all of you, Happy Turkey Day! ANY TIE-INS TO FOOD AND DRINK ARE PURELY INTENTIONAL, TO INCREASE YOUR APPETITE! |

| Printer Friendly | Permalink | | Top |

| muriel_volestrangler

|

Thu Nov-26-09 08:44 AM Response to Original message |

| 1. Dubai debt worry ripples across assets |

|

Debt problems in Dubai hit global stocks, helped lift bonds and took the dollar away from a 14-year low against the yen on Thursday. Gold climbed to a new record high before falling back as the dollar rose. ... Dubai said on Wednesday it was asking creditors of Dubai World and property group Nakheel to agree a debt standstill as it restructures Dubai World, the conglomerate that spearheaded the emirate's breakneck growth. ... There were sharp losses in Europe, where the pan-European FTSEurofirst 300 index .FTEU3 fell more than 2 percent. http://www.reuters.com/article/businessNews/idUSTRE5AN54C20091126 London Stock Exchange trading hit by technical glitch Trading on the London Stock Exchange (LSE) has been brought to a halt by technical difficulties. The LSE said it had been affected by connectivity issues and at 1033 GMT had placed all orders for shares into an "auction call period". ... The FTSE 100 index of leading shares was down 99.84 points, or 1.9%, at 5,264.97 when trading was interrupted. Share markets across the world have been trading lower on Thursday after the investment company Dubai World asked for a six-month delay on repaying its debts, raising concerns about Dubai's financial health. http://news.bbc.co.uk/1/hi/business/8380607.stm It's been closed for 3 hours now. |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 08:46 AM Response to Reply #1 |

| 3. Very Interesting |

|

First the FAA, now the London Stock Exchange....

|

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 09:05 AM Response to Reply #3 |

| 8. Here's Another: Ebay site crashes due to surge in listings |

|

http://www.ft.com/cms/s/0/905f1d70-d766-11de-b578-00144feabdc0.html

Ebay became a victim of its own success at the weekend after a surge in the number of items for sale caused the world�s largest online auction site to crash. Millions of shoppers were first unable to search for items on the website on Saturday, during the crucial weeks before Christmas, after a computer system failure. Ebay said there had been a huge rise in the number of items listed for sale on its site in the run-up to the holiday season this year. It currently has more than 200m live listings, 33 per cent more than at this time last year. On Sunday, the company�s website still said it was working to resolve the technical problems, which had first been noticed at about 11am Pacific Standard Time on Saturday. It will be one of the worst outages suffered by the company in recent years. Ebay could be left with a hefty bill to compensate sellers for losses caused by the outage....Many sellers have complained that they received much lower prices for their goods because people were unable to bid.... The number of merchants selling items on the site usually rises in the weeks before Christmas, but this year�s rise has been particularly steep because Ebay has encouraged large retailers to sell through the site, which until recently was the preserve of individuals and smaller retailers. Some existing sellers have criticised the policy for putting a strain on the system. In its early days of operation, about 10 years ago, Ebay suffered frequent computer failures, but it has been more reliable recently. �This is the certainly the worst for a long time,� said Mr Holland. �It will affect people more than 10 years ago, because there are so many people now who depend on selling through Ebay for their livelihood.� |

| Printer Friendly | Permalink | | Top |

| muriel_volestrangler

|

Thu Nov-26-09 12:08 PM Response to Reply #1 |

| 40. London index closed down 3.2% - biggest fall since March |

|

The UK's FTSE 100 index lost 3.2%, its biggest one-day fall since March, after Dubai World asked creditors to postpone upcoming repayments until May 2010. Banks were hit particularly hard on concerns over Dubai's ability to pay back its debts. ... French and German shares also declined, with France's Cac index ending down 3.2%, and Germany's Dax losing 3.4%. http://news.bbc.co.uk/1/hi/business/8381258.stm Dubai not too big to fail? Dubai is not too big to fail. That seems to be the message of the surprise 6 month debt standstill at Dubai World, the most indebted offshoot of the UAE's most indebted emirate. International markets have been jarred by the news, perhaps as much by the timing as the decision itself (US investors, with markets closed for Thanksgiving, feel more vulnerable than most). But if you have a lot of money resting on Dubai coming through their dramatic boom and bust story intact, this is indeed a major shock. Put simply: everyone in the markets thought that, in the end, the federal government in Abu Dhabi would stand by all of Dubai's bad bets. Apparently, they won't. http://www.bbc.co.uk/blogs/thereporters/stephanieflanders/2009/11/dubai_not_too_big_to_fail.html |

| Printer Friendly | Permalink | | Top |

| Ghost Dog

|

Thu Nov-26-09 02:33 PM Response to Reply #1 |

| 42. Thanksgiving No Holiday for World Markets (Big news, Large moves) |

|

LONDON, Nov. 26, 2009 Thanksgiving No Holiday for World Markets

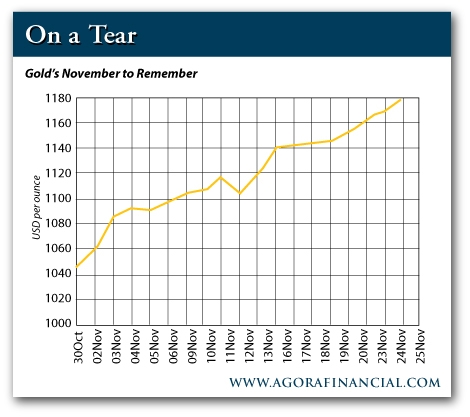

Stocks Tumble Overseas Amid Fears over Dubai Investment Firm and Weak U.S. Dollar (AP) World stock markets tumbled Thursday as investors fretted over the debt problems at Dubai World, a government investment company, and the continuing slide in the dollar, which earlier fell to a 14-year low against the yen. Markets are usually relatively quiet when Wall Street is closed for a holiday, as it is Thursday for Thanksgiving Day. Not so today, as the rest of the world digested the stunning news from Dubai that the government's flagship investment company was in financial trouble. European markets followed Asia lower with the FTSE 100 index of leading British shares closing down 170.68 points, or 3.2 percent, at 5,194.13, having been out of action earlier for over three hours because of technical problems. Germany's DAX fell 188.85 points, or 3.2 percent, to 5,614.17 while the CAC-40 in France was 129.93 points, or 3.4 percent, lower at 3,679.23. Sentiment in stocks was dented by the news that Dubai World, which is thought to have debts totaling around $60 billion, has asked creditors if it can postpone its forthcoming payments until May. That stoked fears of a potential default and contagion around the global financial system, particularly in banks and emerging markets. ... Banks bore the brunt of the selling in Europe, amid fears of potential exposure to Dubai. In London, Royal Bank of Scotland PLC was down nearly 8 percent, making it the biggest faller on the FTSE. In Germany, Deutsche Bank was the biggest faller on the DAX, down around 6 percent. Investors were also keeping a close eye on associated developments in the currency markets after the dollar slid to a new 14-year low of 86.27 yen, while the euro pushed up to a fresh 15-month high of $1.5141. By late afternoon London time, the dollar had recouped some ground and was trading at 86.55 yen, down 0.9 percent on the day, while the euro was 1 percent lower at $1.4988. The continued appreciation in the value of the yen continued to dent Japanese stocks as investors worry that the rising currency will have a detrimental effect on the country's exports. Japan's Nikkei 225 stock average fell 58.40 points, or 0.6 percent, to 9,383.24. Kit Juckes, chief economist at ECU Group, said the developments in Dubai and in the currency markets are related as the fall in risk appetite has pushed money into government bonds and into safe haven currencies such as the Swiss franc and the yen. This, he said, is "testing the tolerance of central banks to see their currencies cause further damage to their economies." Already there have been unconfirmed reports that the Swiss National Bank has intervened to buy dollars to prevent the export-sapping appreciation of the Swiss franc. ... Across all markets, there is a growing awareness that investors may use the upcoming year-end to lock-in whatever profits have been made over the last 12 months. Gold has been one of the biggest high-flyers over the last few months, having gained over 10 percent in November alone. It continued to rise Thursday as investors bought it up as a safe haven. It hit a new record high earlier of $1,196.8 an ounce, before falling back modestly. By late afternoon London time, gold was down 0.4 percent at $1,182.50 an ounce. Oil also fell alongside stocks - the two have traded alongside each other for much of this year. Benchmark crude for January delivery was down $1.85, or 2.4 percent, at $76.11 a barrel. On Wednesday, it rose $1.94. Earlier in Asia, the Shanghai index tanked 119.19 points, or 3.6 percent, to close at 3,170.98, its biggest one-day fall since August 31, while Hong Kong's Hang Seng shed 1.8 percent to 22,210.41. Elsewhere in Asia, markets in Australia, Singapore, Taiwan and Indonesia closed lower. /... http://www.cbsnews.com/stories/2009/11/26/business/main5788522.shtml |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 08:44 AM Response to Original message |

| 2. Dilbert Bastes the Turkeys from His Cubicle |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 10:59 AM Response to Reply #2 |

| 33. And Somebody set It to Song |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 08:50 AM Response to Original message |

| 4. Recession to leave permanent scars |

|

http://www.ft.com/cms/s/0/9cedc026-d858-11de-b63a-00144feabdc0.html

On a blustery November morning at an airfield outside London, an enormous second-hand car auction is buzzing; demand is so great that average prices have risen 27 per cent over the past year. �The turnround started in January and we haven�t looked back since,� says Tim Naylor of British Car Auctions. The global recovery is now evident across the world. The risk of a double-dip recession remains. In recent weeks, though, the US, eurozone and Japan have all reported that their economies grew again in the third quarter. Some trade-dependent economies are setting records as they bounce back. Singapore has enjoyed the fastest rise in national income over the past six months since quarterly records began in 1975. But though the recovery is real, so are the scars from the global recession. Some will be permanent and many will heal only very slowly. From global output on a persistently lower path than expected before the crisis, to severely weakened public finances, to the evils of long-term unemployment, to rising inequality and to a permanently altered balance of global economic power, the effects of the 2008-09 financial crisis and recession are akin to those of a war. Carmen Reinhart of the University of Maryland, who has jointly compiled the definitive history of financial exuberance followed by crisis with Kenneth Rogoff of Harvard University, says: �More money has been lost because of the four words �This time is different� than at the point of a gun.� Spanish unemployment at almost a fifth of the workforce with a budget deficit expected to reach 10 per cent of national income is just one legacy of the culture of easy credit-fuelled growth followed by last year�s collapse. In California, neighbourhoods in cities such as Palmdale and Lancaster have been left empty because of mortgage foreclosures that have continued unabated. Unemployment across the state � the most populous in the US � is running at more than 12 per cent, and the state�s budget is in crisis. The economics profession, so adept at chronicling the �Great Moderation� of economic shocks since the mid-1980s, has been forced to shelve this work. Delving deeper into history and scanning a wide horizon, it is producing evidence and clues about how lasting the scars are likely to be. The emerging consensus � for the advanced world at least � is that they will be deep and long-lived. In its recent World Economic Outlook, the International Monetary Fund examined 88 banking crises between 1970 and 2002 and found, on average, that countries do not earn back all the lost ground after the recession slips into people�s memories. In its database, it found that seven years after a crisis, output had fallen by 10 per cent compared with the pre-crisis path. Economic growth generally returned to the pre-crisis rate, but the loss of output seems permanent. This average result is far from uniform, but the persistent output loss was statistically significant and, in 90 per cent of the banking crises it studied, ranged between 7 per cent and 13 per cent. After seven years, the IMF found that three separate and equally-sized forces tended to prevent economies rebounding to their pre-crisis trends. First, the employment rate is persistently lower, as the pre-crisis boom sucked labour into parts of the economy � such as residential construction in the US � which is no longer required in large numbers. Reallocation of labour across sectors takes time and if the initial surge in unemployment persists, former employees lose skills, contacts and attachment to working. These losses are permanent. Second, the capital stock takes a permanent knock as some plant and equipment is scrapped prematurely, while other companies struggle to invest in viable projects because banks restrict credit to shore up their finances. Third, labour and capital tend to combine to produce less than before, perhaps because innovative companies cannot raise capital or, as the IMF says, �productivity may also suffer due to less innovation, as research and development spending tends to be scaled back in bad times�. These effects were particularly important for countries with high investment rates before the crisis. From his joint analysis of financial crises over 800 years, Prof Rogoff told US radio: �These are very traumatic events. They have political consequences that you can see for decades. They have profound consequences on how the economy is structured. This is going to influence a whole generation that�s been through this.� The sober tone of studies of past banking crises is evident in a study published last week in the Organisation for Economic Co-operation and Development�s Economic Outlook. Although it calculates the initial effect of the crisis on potential output is only 3.5 per cent, this comes at a time when rich country economic speed limits are �still expected to slow from the 2-2� per cent a year achieved over the seven years before the crisis to around 1� per cent in the medium-term, primarily reflecting the impact of ageing populations on potential employment growth�. Not all economists are so certain the scars are inevitable. Drawing on Rogoff and Reinhart�s book title This time is different, Stephen Cecchetti, Marion Kohler and Christian Upper argue on VoxEU.org that this crisis has little in common with those studied by others. �The current crisis is less similar to all of the crises in our database than, say, the Japanese financial crisis of the 1990s is to either the crisis experienced by Ecuador in 1998 or the one that took place in Bulgaria during the transition,� they write, predicting that the particular circumstances of this recession suggests output should reach its pre-crisis level by the second half of 2010. That would represent a much faster recovery in advanced economies than expected. But even so, they do not think the scars will heal quickly. �Regardless of whether crisis-country output returns to its pre-crisis level slowly or quickly, it is still likely to have lasting costs,� they say. |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 08:53 AM Response to Reply #4 |

| 6. US GDP growth revised down to 2.8% |

|

http://www.ft.com/cms/s/0/2b70671c-d8fa-11de-99ce-00144feabdc0.html

US gross domestic product grew at an adjusted annual rate of 2.8 per cent, the commerce department said on Tuesday, down from a previously estimated expansion of 3.5 per cent, but still breaking a dire stretch of four straight quarters of contraction. The revision was in line with economists� estimates, reflecting weaker consumption, a rise in imports and slimmer non-residential investment. Consumer spending grew by 2.9 per cent, down from the 3.4 per cent that was originally reported.... |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 08:51 AM Response to Original message |

| 5. Irish public sector workers strike |

|

http://www.ft.com/cms/s/0/68b1bb6c-d8ff-11de-99ce-00144feabdc0.html

Irish government employees staged their biggest strike in at least three decades on Tuesday, with about 250,000 workers protesting against plans to cut pay to contain the budget deficit. All schools were closed. Hospitals cancelled elective surgery appointments. All but emergency services faced disruption as nurses, teachers, firefighters and other state employees joined the stoppage against plans to cut �1.3bn (�1.7bn, $1.9bn) from the public sector pay bill... |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 08:57 AM Response to Original message |

| 7. AIG and Greenberg settle dispute |

|

http://www.ft.com/cms/s/0/3f857e9a-da17-11de-b2d5-00144feabdc0.html

AIG and Hank Greenberg have agreed to settle all the remaining lawsuits between them, in a deal that will see the insurer return a Persian rug and photographs of its former chief executive with Chinese leaders and the company�s founder. The US insurer, rescued last year with more than $180bn (�108bn) of government money, will reimburse legal fees of up to $150m for Mr Greenberg and Howard Smith, AIG�s former chief financial officer, subject to a review by an independent third party. The settlement also covers CV Starr, an insurance firm headed by Mr Greenberg that underwrote some of AIG�s business, and Starr International Company, his private investment group. Mr Greenberg will retrieve photographs of himself with Cornelius Vander Starr, the group�s founder, and with Chinese authorities in AIG�s Shanghai building. The settlement enables Mr Greenberg to write his memoirs, by giving �reasonable access to, and/or copies of� archival materials. Both sides agreed not to make public statements disparaging the other, ending a period of hostile exchanges after Mr Greenberg�s departure when AIG was hit by an accounting scandal in 2005. In August, Mr Greenberg and other former AIG executives agreed to pay $115m to settle shareholder lawsuits over the 2005 restatement of its accounts, people familiar with the situation said at the time. Mr Greenberg also won a jury ruling in July after AIG had claimed that Starr International was liable for $4.3bn of shares held for a now-terminated AIG compensation plan. AIG, 80 per cent owned by the government, said that it was pleased to settle the matter. �The resolution of these long-running disputes will remove a significant distraction and expense and allow AIG to better focus its efforts on paying back taxpayers and restoring the value of our franchise for the benefit of all our stakeholders,� said Robert Benmosche, AIG�s chief executive. �I want to express my appreciation for Bob Benmosche�s help, and the help of the AIG board, in resolving them,� said Mr Greenberg. �I look forward to assisting AIG in trying to preserve and restore as much value as possible for all of AIG�s stakeholders.� |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 09:09 AM Response to Original message |

| 9. Bets rise on rich country bond defaults |

|

http://www.ft.com/cms/s/0/f4f9a4f0-d791-11de-b578-00144feabdc0.html

The mounting level of debt in the industrialised world is prompting a growing number of investors to use the derivatives market to bet on the chance of rich governments defaulting on bonds. The volume of activity in sovereign credit default swaps � which measure the cost to insure against bond defaults � linked to the US, UK and Japan have doubled in the past year because of concerns about their public finances. CDS volumes for Italy, which has one of the highest debt burdens of the developed economies, are now the highest for an individual country, according to the Depository Trust & Clearing Corporation. In contrast, the outstanding volume of CDS linked to emerging nations such as Russia, Brazil, Ukraine and Indonesia have been flat or fallen in the past 12 months as investors have become less interested in trading the risks of those countries. In the past, the CDS market for developed countries was sluggish, because few investors saw the need to buy or sell protection against a risk of default that seemed exceedingly remote. However, rising debt levels and growing political and economic uncertainty have created a more active market, with more investors now seeking insurance. Meanwhile, many banks are prepared to offer protection in exchange for a fee. This fee has recently jumped, since the cost to insure the debt of developed countries has increased since the summer of last year, while the cost of insuring emerging market debt has fallen. Gary Jenkins, head of fixed income research at Evolution, said: �The biggest single risk hanging over the bond markets is the rapid rise in public debt in the industrialised world. �If we get to a point where the market thinks the levels of debt are unsustainable, then we will see an almighty sell-off in the government bond markets, with yields soaring. Governments need to take action to cut deficits and debt.� Fitch Solutions, the data arm of the Fitch Group, said that there was almost as much uncertainty in the CDS market about the outlook for the developed economies and their bond markets as there was for emerging economies. Comparisons between Italy and Brazil are often used by strategists as an example of the contrasting fortunes of the developed and emerging world. Italy�s ratio of debt to gross domestic product is forecast to rise to 127.3 per cent in 2010. On the other hand, Brazil�s debt-to-GDP ratio is forecast to stabilise at 65.4 per cent in 2010. Nigel Rendell, senior emerging markets strategist at RBC Capital Markets, said: �It is not surprising that investors are increasingly worried about debt in the industrialised world. Debt to GDP of more than 100 per cent is difficult to sustain.� |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 09:18 AM Response to Reply #9 |

| 13. See Dubai Posting upthread |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 09:12 AM Response to Original message |

| 10. CARE FOR A BEVERAGE? Coca-Cola aims to triple China sales |

|

Edited on Thu Nov-26-09 09:21 AM by Demeter

http://www.ft.com/cms/s/0/b860d1ee-d79b-11de-b578-00144feabdc0.html

Coca-Cola is planning to more than double its number of bottling plants in China in the coming decade as part of its aim to triple the size of its sales to the country�s rapidly emerging middle class....Coca-Cola�s plans to expand in China are a central part of its push to double revenues � and those of its bottlers � from almost $100bn now to $200bn in the next 10 years ARE THEY NUTS? THAT'S A RIDICULOUS PLAN. Coca-Cola executives say they expect 60 per cent of the new growth to come from China, India and other emerging markets, with only 15 per cent from developed markets. China, already Coca-Cola�s third-largest national market by revenues, has an average per capita consumption of 28 Coca-Cola products per year � on a par with poor African countries and well below the 199 Coca-Cola products per capita drunk last year in Brazil. |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 09:14 AM Response to Original message |

| 11. S&P raises fears over health of some banks |

|

http://www.ft.com/cms/s/0/d9944da0-d863-11de-b63a-00144feabdc0.html

A study by Standard & Poor�s, one of the world�s leading credit ratings agencies, has raised questions over the financial strength of some of the biggest banks ahead of new rules that could require them to raise more funds. The analysis by S&P showed that HSBC is the best capitalised bank in the world, while Switzerland�s UBS, Citigroup of the US and several of Japan�s biggest banks are among the weakest. The ranking of 45 of the world�s leading banks will unnerve investors, highlighting once again the capital shortfall that institutions still need to make up over the coming years. Although some banks will be able to top up capital through retained profits, analysts expect a string of rights issues from weaker banking groups as they try to raise tens of billions of dollars. S&P�s risk-adjusted capital (RAC) ratios � a measure of balance sheet strength � foreshadow the new capital ratio regime expected to be set by the Basel committee on banking supervision early next year. Its report, published on Monday, gave HSBC a 9.2 per cent ratio, compared with barely 2 per cent for the likes of UBS, Citigroup and Mizuho. The assessment, which measured banks� financial strength at the end of June, offered a different picture of banks� relative strength to that under the current �Basel II� rules on capital adequacy. Under existing rules, UBS had an end-June �tier one� ratio � the standard measure of capital strength � of more than 13 per cent, compared with 10 per cent for HSBC. The RAC ratio reflects banks� leverage � asset volumes as a proportion of equity � and factors in greater risk-weightings on assets. Bernard de Longevialle, who led the analysis, said: �Our study shows that capital for the majority of banks remains a relative weakness.� Only nine of the 45 banks studied had a ratio above 8 per cent, the minimum level to cover forecast levels of stress. The S&P ratio strips out national peculiarities, such as regulatory authorisation for high levels of hybrid debt in a bank�s capital make-up, dragging down the ratios of Japanese, German and Swiss banks. S&P plans to use its RAC ratio as an element of future credit ratings analysis. Basel II rules are currently being overhauled and are expected to move away from current definitions of �core tier one�, which measures equity strength, and �tier one�, which ranks capital instruments such as hybrid debt virtually on a par with equity. Risk weightings applied to certain assets will also be increased. |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 10:58 AM Response to Reply #11 |

| 32. Quelle Surprise! Most Big Banks Lack Capital By Edward Harrison |

|

http://www.nakedcapitalism.com/2009/11/quelle-surprise-most-big-banks-lack-capital.html?utm_source=feedburner&utm_medium=email&utm_campaign=Feed%3A+NakedCapitalism+%28naked+capitalism%29

My post title is an ode to Yves Smith, who likes to feign surprise when the blindingly obvious finally comes into plain view for all to see. The latest sign that underneath the surface weakness remains at large financial institutions comes courtesy of Standard & Poors. According to the Telegraph�s Ambrose Evans-Pritchard, S&P believes many are horribly short of capital. Every single bank in Japan, the US, Germany, Spain, and Italy included in S&P�s list of 45 global lenders fails the 8pc safety level under the agency�s risk-adjusted capital (RAC) ratio. Most fall woefully short. The most vulnerable are Mizuho Financial (2.0), Citigroup (2.1), UBS (2.2), Sumitomo Mitsui (3.5), Mitsubishi (4.9), Allied Irish (5.0), DZ Deutsche Zentral (5.3), Danske Bank (5.4), BBVA (5.4), Bank of Ireland (6.2), Bank of America (5.8), Deutsche Bank (6.1), Caja de Ahorros Barcelona (6.2), and UniCredit (6.3). While some banks may look healthy under normal Tier 1 and leverage targets, critics claim these measures can be highly misleading since they fail to discriminate between high-risk and low-risk uses of leverage. The system failed to pick up the danger signals before the financial crisis. The supposedly moderate leverage of US banks in 2007 proved to be a spectacularly useless indicator. This shouldn�t come as a shocker. Recently, I mentioned that Citigroup was well-capitalized according to standard metrics due to government bailout money. But questions linger about whether this profile masks large holes in Citi�s balance sheet. Irrespective, Credit Suisse believes that regulatory hurdles for Citigroup will restrict its earnings potential. The S&P article bears this out. S&P has shifted to a tougher code. It is less tolerant of hybrid capital � a liability rather than an asset, and no defence in a crunch � and insists that banks must quadruple capital put aside to cover trading desks. Private equity exposure will be treated more harshly. The Bank for International Settlements unveiled its own version in September. The regulatory framework worldwide is clearly shifting in this direction, a move that will hit some banks harder than others. "We expect banks to continue strengthening capital ratios over the next 18 months to meet more stringent requirements. Failure to achieve this could put renewed pressure on ratings," said Bernard de Longevialle, S&P�s credit strategist. If S&P understands the weaknesses masked by measures such as Tier 1 capital or even tangible common equity as proxies for bank health, I suspect national regulators do as well. However, the recovery to date has been built on the back of avoidance of this unpleasant fact lest we risk a renewed bout of panic and another downturn. Under no circumstances do policy makers want large financial institutions to be subject to tougher regulations before they have rebuilt capital via government purchases of toxic assets, government backstops, low interest rates, and a steep yield curve. Tougher rules at this juncture may prove "pro-cyclical", if banks respond by cutting loans. This may perpetuate the credit crunch for smaller borrowers unable to tap the bond markets. "There is a risk that the increase in regulatory capital requirements could weigh on banks� ability to finance recovery," said Mr de Longevialle. Below is a list of the safest institutions according to S&P. While I expected to see HSBC and Standard Chartered on the list, Santander is a notable absence. Also a bit surprising, Deutsche Bank, generally deemed to have weathered the storm (despite large CRE exposure), is one of the weakest, not the strongest. I never would have expected Dexia, ING and Barclays to be on the list of strongest. And Nordea still has large exposure to the Baltics. But ING and Dexia have received large bailouts from the Benelux governments. See my list of bank writedowns for specific events by institution. The "safest" global bank is HSBC (9.2), followed by Dexia (9.0), ING (8.9) and Nordea (8.8). UK banks fare relatively well: Standard Chartered (8.1) is in the top quintile; Barclays (6.9) is in the middle. The study left out RBS and Lloyds because their status is unclear. Chinese banks � the world�s largest � were excluded. On the whole, this report leaves me more convinced than ever that a double dip recession would tip us into a 1931-style panic. When I make the Obama-Hoover analogy, this is what I am referring to. As Barack Obama pushes forward with his deficit reduction scheme, perhaps 1931 should be top of mind more than 1937 � or 1994 as seems to be the case for him. |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 09:16 AM Response to Original message |

| 12. Fortune Cookie from Sun Tzu (for the White House) |

|

"In all history, there is no instance of a country having benefited from

prolonged warfare. Only one who knows the disastrous effects of a long war can realize the supreme importance of rapidity in bringing it to a close.": Sun Tzu- (c.500-320 B.C.) name used by the unknown Chinese authors of the sophisticated treatise on philosophy, logistics, espionage, strategy and tactics known as 'The Art of War' - Source: The Art of War |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 09:19 AM Response to Original message |

| 14. Obama and GOP differ over recipe for jobs, economy |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 09:25 AM Response to Original message |

| 15. In Debt We Trust - America Before the Bubble Bursts VIDEO 1.5 HOUR |

|

Edited on Thu Nov-26-09 09:26 AM by Demeter

In Debt We Trust is the latest film from Danny Schechter, "The News Dissector," director of the internationally distributed and award-winning WMD (Weapons of Mass Deception), an expose of the media's role in the Iraq War.

The Emmy-winning former ABC News and CNN producer's new hard-hitting documentary investigates why so many Americans are being strangled by debt. It is a journalistic confrontation with what former Reagan advisor Kevin Phillips calls "Financialization"--the "powerful emergence of a debt-and-credit industrial complex." http://www.informationclearinghouse.info/article17267.htm |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 09:27 AM Response to Original message |

| 16. Still Doing God�s Work on Wall Street By Robert Scheer |

|

http://www.truthdig.com/report/item/still_doing_gods_work_on_wall_street_20091125/

Jail, anyone? Perhaps that�s too harsh, and at any rate premature, but is anyone ever going to be held accountable for the behind-the-scenes sweetheart deals that passed tens of billions of taxpayer dollars through the AIG shell game to the very banks that caused the financial meltdown? Or for the many other acts of double-dealing that left one out of three American homeowners owing much more than their houses were worth while the folks who swindled them were rewarded with hundreds of billions in public money? Undoubtedly not, since the same folks who are most culpable wrote the laws that made this, and the other scams at the heart of the banking collapse, perfectly legal. And guess what? They�re back at work in the government, writing the new laws that will, they claim, prevent us from being had once again. As a telling example of that process at work, check the official response of the Department of Treasury to the devastating report by the special inspector general for the Troubled Asset Relief Program (TARP), Neil M. Barofsky, titled �Factors Affecting Efforts to Limit Payments to AIG Counterparties.� The main factor was that Timothy Geithner followed the lead of Goldman Sachs CEO Lloyd �I�m Doing God�s Work� Blankfein in crowding the lifeboats with bankers. Geithner, now treasury secretary, was previously the president of the Federal Reserve Bank of New York (FRBNY), where he negotiated the deal to pay Goldman Sachs and the other top banks in full to cover their bad bets on securitized mortgages. Barofsky�s report concluded that Geithner�s scheme represented a �backdoor bailout� for the financial hustlers at the center of the market fiasco. Noting that Geithner denies that was his intention, the report states, �Irrespective of their stated intent, however, there is no question that the effect of FRBNY�s decisions�indeed, the very design of the federal assistance to AIG�was that tens of billions of dollars of Government money was funneled inexorably and directly to AIG�s counterparties.� Not surprisingly, the Treasury Department that Geithner now heads defended his actions in not forcing �haircuts� on the full dollar-for-dollar payoff by AIG to the banks while he was at the New York Fed: �The government could not unilaterally impose haircuts on creditors, and it would not have been appropriate for the government to pressure counterparties to accept haircuts by threatening to retaliate in some way through its regulatory power.� Nonsense, argues Eliot Spitzer, who as New York attorney general was way ahead of the curve in challenging Wall Street arrogance. Writing in Slate on Monday, Spitzer points out: �Pressuring Goldman and the other counterparties to offer concessions would have forced them to absorb the consequences of making suspect deals with an insurance company that was essentially a Ponzi scheme.� The Ponzi scheme was based on the collateralized debt obligations (CDOs) in which the bankers traded and which AIG had insured with the credit default swaps (CDSs) that they sold but failed to back with adequate funding. Now Geithner�s Treasury concedes that AIG �should never have been allowed to escape tough, consolidated supervision.� But none of AIG�s scams were regulated, nor were any of the others at the center of the larger financial debacle, because of laws pushed through Congress by Geithner�s boss, Lawrence Summers, when they both were in the Clinton administration. Specifically, they prevented regulation of those opaque CDOs and CDSs that would come to derail the world�s economy. As the inspector general�s report stated: �In 2000, the Sounds nonsensical today: The inspector general�s report notes that AIG, because of the deregulatory law that Summers and Geithner pushed through, was �able to sell swaps on $72 billion worth of CDOs to counterparties without holding reserves that a regulated insurance company would be required to maintain.� But why, then, is Summers once again running the show with Geithner when both have made careers of exhibiting total contempt for the public interest? Because there is no accountability for the high rollers of finance, no matter who happens to be president. |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 09:41 AM Response to Reply #16 |

| 17. Geithner, under fire, defends AIG bailout |

|

http://www.reuters.com/article/newsOne/idUSTRE5AI2Z820091119

By David Lawder and Emily Kaiser WASHINGTON (Reuters) - U.S. Treasury Secretary Timothy Geithner on Thursday defended the costly bailout of insurer AIG and urged swift regulatory reform to safeguard the economy from the failure of big financial firms. Before Congress' Joint Economic Committee, Geithner faced fierce criticism of his role in the rescue of American International Group Inc (AIG.N) in 2008, when he was president of the New York Federal Reserve Bank. Geithner said AIG's failure posed as significant a risk to the economy as the collapse of investment bank Lehman Brothers, which sparked a panic that froze global trade and threatened to topple the entire financial system. "The United States of America ... came into this crisis without anything like the basic tools countries need to contain financial panics," he said. "Coming into AIG, we had basically duct tape and string." The AIG bailout has become a symbol of outrage over the failings of Wall Street and the government's $700 billion bailout fund, complicating the White House's efforts to get a regulatory reform bill passed. Congress has been wrangling over how best to revamp financial rules to give the government tools to prevent another crisis, while striking the right balance between clamping down on risky lending and hampering the flow of credit. The U.S. House of Representatives Financial Services Committee has been working on a bill for weeks, and the Senate Banking Committee kicked off a similar effort on Thursday. Senator Richard Shelby, the top Republican on the Senate panel, said he would not support a bill put forward by Senator Christopher Dodd, the Democrat who chairs the committee, and called for a "complete rewrite. PRESSURE ON BAILOUTS, CHINA Geithner said because the United States had no authority to seize and wind down complex financial firms that were in danger of collapse, it had no choice but to step in when the failure of AIG appeared imminent in September 2008. A jump in the unemployment rate to above 10 percent has sparked complaints that Washington was quick to rescue Wall Street but ignored the plight of those who lost their jobs in a recession blamed partly on reckless lending. Representative Peter DeFazio, an independent-minded Democrat from Oregon, told MSNBC television on Wednesday that Geithner should not be in his job. At the hearing on Thursday, Representative Kevin Brady, a Republican, similarly called for Geithner's resignation over his handling of the economy and AIG. "Conservatives agree that as point person, you failed. Liberals are growing in that consensus as well," Brady said during a tense exchange with Geithner. "For the sake of our jobs, will you step down from your post?" Geithner responded by defending the actions he and others in the Obama administration took to restore financial calm and economic growth, and the White House later rose to his defense. "Secretary Geithner has helped steer the American economy back from the brink," said White House spokeswoman Jennifer Psaki. "We invite anyone with good ideas, whether they agree with us or not, to be a part of the productive effort toward (an economic) solution." In another tense moment, Senator Charles Schumer, a Democrat, criticized Geithner for treading too softly on the controversial issue of China's yuan currency, which Schumer has long argued is intentionally undervalued. Schumer and Senator Lindsey Graham, a Republican, on Thursday (NOV 19) asked the U.S. Commerce Department to investigate whether China was manipulating its currency to give it a trade advantage. Geithner used his testimony to press the case for action on reforms before momentum faded and argued that the largest institutions need oversight from a single, strong regulator. "The regulation of the largest, most interconnected firms requires tremendous institutional capacity, clear lines of authority and single-point accountability. This is no place for regulation for council or by committee," he said. As part of a sweeping reform plan, the Obama administration has proposed that the Federal Reserve be given powers to oversee the largest firms. Geithner's comments signaled opposition to proposals to give that authority to a council of existing regulators instead of to the central bank. (Additional reporting by Rachelle Younglai; Editing by Padraic Cassidy and Dan Grebler) |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 10:31 AM Response to Reply #17 |

| 28. Government Admits AIG Folly By Ian Mathias |

|

http://dailyreckoning.com/government-admits-aig-folly/

Brace yourselves for a shocking report from the U.S government: After months of research and we don�t even want to know how much money, an independent investigator has concluded that the government wasted a ton of money bailing out AIG. You don�t say! Special Inspector General Neil Barofsky, the man tasked with policing the TARP, released a report last week that focused on the transactions between the New York Fed, led by Tim Geithner, and AIG�s counterparties. As was evident to, ummm� everyone, Barofsky concluded that the Fed blew it by not demanding any concessions from the major holders of AIG credit default swaps � like Hank Paulson�s alma mater, Goldman Sachs. The N.Y. Fed paid out these contracts in full even though they would have been worth far less had Mr. Geithner not stepped in and bailed out AIG. That cost the American taxpayer �tens of billions of dollars,� the report finds. �Geithner�s already tattered reputation took a major blow with his investigation,� Dan Amoss notes. �He does not come out looking so good. I wouldn�t be surprised if President Obama replaced Geithner in 2010, given the mounting evidence that he was handing out taxpayer money and guarantees willy-nilly during the 2008 AIG panic. �With more information about the performance of loans and mortgages in the coming months, the market�s attention could easily shift back to the capital adequacy of the U.S. banking system. And with waning political support for government subsidies, bank executives may have to start taking their lumps the old-fashioned way: raise as much dilutive equity capital as necessary to absorb credit losses. Bank shareholders and bondholders � not taxpayers � should be responsible for their own lending follies. �Bank stocks are among the riskiest stocks to own.� FROM HIS LIPS TO GOD'S EAR |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 11:02 AM Response to Reply #28 |

| 34. Goldman/AIG Conspiracy Theories: There�s a Reason They Won�t Go Away |

|

http://www.nakedcapitalism.com/2009/11/goldmanaig-conspiracy-theories-theres-a-reason-they-wont-go-away.html?utm_source=feedburner&utm_medium=email&utm_campaign=Feed%3A+NakedCapitalism+%28naked+capitalism%29

Note: this post is by Thomas Adams, at Paykin Krieg and Adams, LLP, and a former managing director at Ambac and FGIC, with some minor additions by yours truly. This is a significant piece of some puzzles he, some other experts who prefer to remain anonymous, and I have been pushing on for several months. As we have been reading the latest coverage on the AIG bailout from the SIGTARP report and the Treasury Secretary Geithner�s Congressional testimony, a nagging question remains unresolved: why did AIG get bailed out but the monoline bond insurers did not? The business that caused AIG to blow up was the same that caused the bond insurers to blow up � collateralized debt obligations backed by sub-prime mortgage bonds (ABS CDOs). This was actually one of the few business that AIG Financial Products had in common with the monolines. AIG didn�t participate in municipal insurance, MBS or other ABS deals, which were all important for the monolines. Certainly, AIG was larger than any of the bond insurers, but in aggregate, the bond insurers had a tremendous amount of ABS CDO exposure, which at the peak was probably over $300 billion. Despite AIG�s claims to have withdrawn from subprime at the end of 2005, we have identified particular 2006 deals with substantial subprime content that AIG most assuredly did guarantee. In addition, the monolines had exposure to many other assets classes that AIG did not which created chaos for the holders of those bonds when the monolines were downgraded. The chain reaction risk of the bond insurers was arguably greater, when you throw in the damage to the aucton rate securities market, which was rooted in the muni market. In 2007, MBIA had over $650 billion of par insured, Ambac had about $500 billion, FSA had about $380 billion and FGIC had about $300 billion. Throwing in CIFG and XLCA, the total insured par of the monolines was about $2 trillion � this amount certainly would qualify as large enough to be �systemic risk� if the insurers were allowed to fail. In contrast, while AIG�s aggregate insured par was greater, the only portion that really presented a systemic risk exposure was the CDS and structured finance exposures, which had an aggregate par exposure of about $400-500 billion. a persuasive argument could be made that the monolines were just as intertwined in the financial system as AIG and, thanks to their municipal exposure, presented as great or greater a systemic risk to the financial markets and the economy. Yet AIG was bailed out and the monolines were not. So what happened? How did the monolines get dropped and AIG get rescued? The popular reason given has been that AIG was so big that they affected all segments of the economy, whereas the monolines were only midsized and not critical to the economy. i believe that SIGTARP repeated this version of events last week. I understand that Treasury Secretary Geithner last week repeated this notion and added new information � that he was concerned about the cascading risk of AIG�s non CDS exposure. While this produces a bigger par exposure for AIG, these other areas did not have the huge risks of loss, have largely remained functional, and did not have the issue of collateral posting. The risk were at the parent level, at AIG FP; the bulk of AIG�s business was written by regulated subsidiaries whose claims-paying ability would not be impaired by an AIG FP failure. So, in my view, this is a fairly weak, after the fact argument. A more plausible case might be made that AIG also had a securities lending business that had sprung a $20 billion leak, but that wee problem hasn�t gotten much mention in the official defenses. I have a different interpretation. I should note that I am a former employee of a bond insurer, so I admit to a bias. However, I my general perspective had been, until recently, that neither AIG or the bond insurers should have been rescued. When I was at FGIC, Deutsche Bank, Lehman, Bear and UBS were all over my company with sales coverage for CDO deals. But we never heard much from Goldman. I was actually surprised to see that they were so big with John Paulson�s CDO adventures (as recently disclosed in �The Best Trade Ever�), because I never thought they were that big in the CDO market. One big reason I didn�t know Goldman was so big in CDOs � they didn�t work with the monolines. Goldman wanted their counterparties to post collateral so they would have protection against corporate downgrades. The monolines refused to have collateral posting requirements in their CDS contracts. The rating agencies supported them in this position on the argument that maintaining their AAA rating was �fundamental to their business�. AIG, on the other hand, agreed to collateral posting requirements. in fact, they used this as a competitive advantage � they got more business because of it and marketed their flexibility on this issue to the banks. There were two the key distinctions between the monolines and AIG � first, AIG had other businesses, whose losses could threaten AIG�s financial guarantee business while monolines promised to pay claims first, to protect investors. Second, AIG had a history of negotiating before they paid claims (there is an interesting history with a ABS film receivables deal where AIG refused to pay, while the monolines covered similar deals and did not have the same �out� in their policies. this deal did serious damage to AIG�s reputation in the ABS market and shut them out of many deals). So despite their AAA rating, AIG was not as trusted by the structured finance and CDS market � there was a fear that AIG would wiggle out of their obligations in a way that the monolines would not. All of the other banks got comfortable with the monolines not having to post collateral for CDS trades because of their AAA ratings. Goldman never did. Of course, Goldman was one of the few banks that clearly set out to profit from shorting CDOs. They obviously realized that if their CDS counterparty was on the hook for a lot of ABS CDOs that were going to blow up, the insurance provider would likely get downgraded. If the downgrade of the insurer was very likely, the only way the short-CDO strategy worked was if the insurer would post collateral. So Goldman only used AIG, who would provide protection against their downgrade, which Goldman knew would happen because they were stuffing AIG with toxic ABS CDOs. The banks that used the monolines for their ABS CDOs were making a major error by taking on the monoline downgrade risk without protection, especially if they knew that the ABS CDOs were toxic. So I suspect that most of the banks did not really know that the ABS CDOs would be as toxic as they turned out to be. This is, of course, what happened. The ABS CDOs blew up, the bond insurers got downgraded, the banks that used them got crushed because their hedges against their CDO risks were now in jeopardy. A death spiral between the monolines and the banks ensued (the ARS meltdown added to the troubles). Goldman didn�t care, because they had collateral posted by AIG once AIG got downgraded.. All of the banks who faced the monolines had to start considering commutation deals with the monolines because it was obvious the monolines did not have enough capital to cover all of the CDO losses. in these commutations, the banks accepted payments as low as 40 cents on the dollar. Most of the monoline ratings roubles had unfolded earlier in 2008 � many of them had been downgraded, several commutations had already occurred by the time of the AIG bailout. AIG managed to put off the threat of serious downgrade for a long time, despite the junk in their portfolio (as 2008 progressed, it was a mystery to me and many others why the onolines were being downgraded but AIG was not). While AIG had been downgraded to AA some time earlier, this hadn�t caused much of a disruption because the real trigger for collateral posting was if they went below AA. For a variety of reasons, this wasn�t a threat until September of 2008. I hate to get sucked into the vampire squid line of thinking about Goldman, but the only explanation i can think of for why AIG got rescued and the monolines did not is because Goldman had significant exposure to AIG and did not have exposure to the monolines. When it became clear that AIG could face bankruptcy, Goldman�s plan to profit by shorting ABS CDOs was threatened. While they had the collateral posted, thanks to the downgrades, this collateral could be tied up or lost if AIG went bankrupt. This was a real crisis for Goldman � they thought they had outsmarted the subprime market with their ABS CDOs and outsmarted all of the other banks by getting collateral posting from AIG when they got downgraded. But if AIG went away, this strategy would have blown up and cost Goldman billions. All of this is essentially factual and based, for the most part, on public information. As a matter of speculation, i believe that Goldman and their helpers deliberately pumped up the media with the threats that the subprime market posed in order to hasten the collapse of the subprime market. this allowed them to realize their gains sooner from shorting ABS CDOs � they had become impatient waiting for it to blow up. In addition, I believe that Goldman and their helpers � including their many connections with the White House and the Fed � pumped up concerns about the systemic risk that the market was facing from a Lehman and AIG failure, so that they could force the government to step in and bail out AIG. This would also explain why Lehman was not bailed out. Lehman didn�t really matter to Goldman. But the fear created by Lehman�s failure served as a good excuse for why they should rescue AIG. I have been wondering why the sub-prime market blow up led to such a massive crisis when subprime and structured finance had experienced big problems before without the issue of systemic risk and financial market collapse. Certainly, the ABS CDOs were toxic and caused big holes, but not so big that it couldn�t be addressed by an RTC type of clearing system. Various analyst reports of the bad subprime deals (and ABS CDOs) makes it pretty clear that the 2006-2007 vintages were the worst and will probably only create about $500-700 million of aggregate losses. Terrible, but not insurmountable. This leads me to conclude that the bailout was prompted by fear mongering and deliberate strategies and manipulation on the part of Goldman and a few select others, to make sure that AIG would be bailed out to protect their trades in shorting ABS CDOs. i believe that John Paulson benefited from this bailout, on his $5 billon or so of ABS CDOs with AIG. But not as much as Goldman benefited themselves, via Abacus and, perhaps, other deals. AIG, Goldman and ABS CDOs were tied together at the center of the crisis. From Goldman�s perspective, all of the other participants were secondary � they had no exposure to the monolines and they were probably hedged against the other banks. The only loose end was the collateral posted by AIG. The final question that this raises for me: would it have been cheaper for the government and the taxpayer to have bailed out the bond insurers instead of AIG? The total amount of CDOs and credit default swaps that would have needed to be guaranteed would have been smaller. In the number of investors across the market that would have benefited would probably have been larger. The auction rate securities market, the muni market, the investors that held bond insurer exposure to MBS and ABS would have all benefited. None of these markets were aided by AIG�s bailout. But a bond insurer bailout would not have helped Goldman much and the AIG bailout did. Yves here. Note I differ with Tom on how much Goldman could or did pump up subprime fears. A lot of people focused on Jan Hatzius� bearish calls on financial system losses, but quite a few people in a position to know claim that Hatzius is not the sort to take commercially expedient views. But once the asset-backed commercial paper started imploding in August 2007, the officialdom was very much engaged. So if one can connect the dots between Goldman and the fear and loathing that hit the ABCP market (recall all paper was repudiated as in being possibly tainted by subprime), the story becomes very tidy. Update 1:50 PM Another possible gap in this line of thinking are the now-infamous AIG regulatory capital swaps, which allowed European banks to carry much less equity (or put it another way, pump up their balance sheets much bigger than they would have otherwise been). But there has been a remarkable lack of coverage of this issue. That would be one reason to save AIG and not the monolines. There isn�t any evidence that this issue factored into official thinking. That could mean that the officialdom has scrupulously avoided mentioning it (as in why alert the peasants that their tax dollars are supporting profligate Eurobanks), but Sorkin�s Too Big to Fail makes clear that AIG itself was not on top of how badly the ship was leaking, so if AIG didn�t bring this issue up as a need to be rescued, no one would have factored that into their decisions. One way to be certain would be to compel disclosure of the phone logs during the AIG scramble. A absence of calls to European banking regulators would be indirect confirmation that these swaps were not one of the proximate causes of the AIG rescue. |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 11:38 AM Response to Reply #34 |

| 35. Goldman's secret moral pathology |

|

http://www.marketwatch.com/story/15-signs-wall-street-pathology-is-spreading-2009-11-24?siteid=rss&rss=1

15 symptoms of a Wall Street disease destroying democracy and capitalism By Paul B. Farrell, MarketWatch ARROYO GRANDE, Calif. (MarketWatch) -- In "The Battle for the Soul of Capitalism" Jack Bogle no longer sees Adam Smith's "invisible hand" driving "capitalism in a healthy, positive direction." Today, his "Happy Conspiracy" of Wall Street plus co-conspirators in Washington and Corporate America are spreading a contagious "pathological mutation of capitalism" driven by the new "invisible hands" of this new "mutant capitalism," serving their selfish agenda in a war to totally control America's democracy and capitalism. . The "Goldman Conspiracy" is the perfect B-school case study of Wall Street's secret contagious pathology, with insiders like Lloyd Blankfein, Henry Paulson and others pocketing billions more of the firm's profits than shareholders, evidence the new "mutant capitalism" has replaced Adam Smith's 1776 version which historically endowed the soul of American democracy as well as our capitalistic system. Sadly for America Goldman's disease is rapidly becoming a pandemic spreading beyond Wall Street's too-greedy-to-fail banks, infecting our economy, markets and government as it metastasizes globally. What are the symptoms of this growing "soul sickness," this "pathological mutation of capitalism" Bogle fears? Recently we reviewed the consequences of this "soul sickness." Today we'll paraphrase news reports about 15 symptoms spreading "soul sickness" beyond the boundaries of this Goldman case study: These are the 15 signs of a moral pathology undermining not just banking but American democracy and capitalism. 1. Gross denial of any moral damage caused by their rampant greed Seeking Alpha: "Goldman is America's most hated corporation." We cheer as Rolling Stone's Matt Taibbi calls Goldman "a giant vampire squid wrapped around the face of humanity." Banks triggered a global crisis. Main Street suffers. Greedy bank CEOs raid the Treasury then stuff $30 billion in their bonus pockets, up 60% from last year. They are our 21st century General Motors, convinced "What's good for Goldman is good for America." We saw how that arrogance ended. Wall Street has similar suicidal symptoms. 2. Narcissistic egomaniacs with secret 'God complexes' London Times' John Arlidge interviewed Goldman CEO Blankfein: "He paid himself $68 million in 2007, now worth more than $500 million, yet insists he's a blue-collar guy. He says banking has a 'social purpose,' just a banker 'doing God's work.'" When I was at Morgan Stanley in the 1970s the firm ran an ad: "If God Wanted To Do a Financing, He Would Call Morgan Stanley." Today, all of Wall Street is dual diagnosed: They're morally blind money addicts who believe they're "God's chosen." AA would say: They haven't "bottomed," won't recover from their disease till a disaster hits, with another market meltdown and the "Great Depression 2." Then maybe they'll "quit playing God." 3. Paranoid obsessives about secrecy, guilt and non-disclosure Bloomberg: "New York Fed's Secret Deal: Taxpayers paid $13 billion more than necessary when government officials, acting in secret, made deals with banks on AIG, buying $62 billion of credit-default swaps from AIG." The government would eventually cover about $180 billion in AIG swaps backing toxic CDOs when Paulson and Ben Bernanke double-teamed to bailout Goldman, saving them from bankruptcy. 4. Power-hungry need to control government using Trojan Horses Wall Street Journal: "For a year Goldman said it wouldn't have suffered damage if AIG collapsed. But a new report kills that claim. TARP inspector general found that then New York Fed Chair Tim Geithner gave away the farm. If AIG had collapsed, Goldman would have had to cover the losses itself. They couldn't collect on the protection of AIG swaps." Yes, Goldman was bankrupt. But friends in high places always save them. 5. Borderline personalities who regularly ignore conflicts of interest New York Times: "Before becoming Treasury secretary in 2006, Hank Paulson agreed to hold himself to a higher ethical standard than his predecessors. He specifically said he'd avoid his old buddies at Goldman where he was CEO. Later Congress saw many conflicts of interest, not just meetings but favorable treatment for his buddies at Goldman." 6. Pathological liars incapable of honesty even with own investors McClatchy News: "Goldman secretly bet on the U.S. housing crash after peddling more than $40 billion of securities backed by 200,000 risky home mortgages. But they never told their investors they were also secretly betting that a drop in housing prices could wipe out the value of those securities." Paulson knew, stayed silent. "Only later did their investors discover Goldman's triple-A investments were junk. Did Goldman's failure to disclose its bets on an imminent housing crash violate securities laws?" Boston University Prof. Laurence Kotlikoff says: "This is fraud, should be prosecuted." But it won't be in the new "mutant capitalism." Members of AA say you know when an alcoholic is lying: Their lips are moving. Same with Wall Street: Think liar's poker. It's in their DNA. They're compulsive liars trapped in a culture of secrecy. They lie, the lies cascade, memory slips, more lies are necessary, they cannot stop lying. Goldman sure can't ... look, their lips are moving again. 7. Sole fiduciary duty to insiders, not investors, never the public New York Examiner: "Goldman was at the heart of the subprime market, selling subprime junk as no-risk AAA bonds, then gambling, hedging, shorting their investors. Goldman traded like Enron. That set up the meltdown. The Fed and Goldman's ex-CEO at Treasury saved Goldman. Taxpayers got stuck with the bill. Bailout overseer Elizabeth Warren called this reckless gambling. Trend forecaster Gerald Celente calls it mafia-style looting. 8. Moral issues are PR glitches, violations of 'don't get caught' rule USA Today says "Goldman Sachs should be celebrating. Yet, the mood at the investment bank seems to be one of crisis about the public backlash over employees' bonuses." So Goldman's on a PR blitz in a bid to undo the damage. They canceled their Christmas party. Also launched a $500 million program for small businesses. Get it? They can't see their moral failings, only a PR problem, so they hire PR agents and crisis managers first. 9. Charitable donations are tax and PR opportunities, not moral issues New York Times: Examined Goldman charitable foundation's tax filing: Thick as a phone book with more than 200 pages of trades. "Never seen anything like it," said Verne Sedlacek, president of Commonfund, a $25 billion fund for universities and nonprofits. The money to Goldman's foundation is dwarfed by insiders' bonuses. The foundation got $400 million, gave away $22 million. Bonuses were 20 times more. Even the New York Post said "Goldman's Born Again Image is Laughable." They're sleaze-ball cheapskates. 10. When exposed in a massive fraud, feign humility, fake an apology CBS MoneyWatch: "Blankfein now says he's 'sorry for the role Goldman played in the housing crisis: We participated in things that were clearly wrong.'" Wrong? Sounds more like he's admitting to something "clearly criminal." Reread: Isn't he admitting guilt to a fraud; cheating millions of homeowners, shareholders, taxpayers? Then laughs at us with phony "restitution," a fund of $100 million annually for five years to small-business owners. Financial Times says "$100 million is the profits from one good trading day. In 3Q '09 they had 36 days better than that." Unfortunately, these crooks will get away with it. 11. When bankruptcy threatens, bribe friends in 'Happy Conspiracy' Barron's: While Geithner was "showcasing what a great investment Washington made in Goldman, the 23% return on the $5 billion of the taxpayers money, Warren Buffett's deal made him a fabulous 120% return. Goldman's stock ran up to $180 from $115, a gain of $2.8 billion. Add 8% discount on warrants, another $3.2 billion to him." 12. Engage co-conspirators to cover up, distract, do your dirty work Reuters: "Former Merrill Lynch CEO John Thain was fired after a scandal over the billions in Merrill bonuses. He says big insider bonuses don't cause excessive risk-taking nor the financial crisis." He blames "poor risk management, excessive leverage and too much liquidity for too long. But even if they tie bonuses to long-term performance, that won't prevent the next collapse." Why? They'll find new ways to break the moral code. 13. As money-hungry vultures they will prey on vulnerable Americans McClatchy News: "An obscure Goldman subsidiary spent years buying hundreds of thousands of subprime mortgages, many from the more unsavory lenders. They repackaged them as high-yield bonds. The bottom fell out. Now, after years of refusing to disclose they owned the mortgages, the secret is out and Goldman has become one of America's biggest, greediest foreclosers." Yes, the vampire squid wants pounds of flesh. 14. Treat everyone not in the 'Happy Conspiracy' with tough love HuffPost's Leo Leopold warns: "Each day reveals how we've traded away our sense of decency and the common good in exchange for pure greed. Unemployment means hunger. The Agriculture Department reports 49 million Americans don't have enough food, up 13 million over the last year, highest number ever." Wall Street treats anyone not in the "Happy Conspiracy" as morally defective capitalists in need of "tough love." 15. Addicts consumed by money: 'Jesus would throw them out ...' New York Times' Maureen Dowd: "Goldman's trickle-down catechism isn't working. We have two economies. In the past decade Wall Street's shared little with society. Their culture is totally money-obsessed. There's always room for a bigger house, bigger boat. If not, you're falling behind. It's an addiction. And Washington's done little to quell it. Geithner coddles wanton bankers. Obama's absent. 'Saturday Night Live' was tougher. And as far as doing God's work: The bankers who took taxpayer money, pocketing obscene bonuses: They're the same greedy types Jesus threw out of the temple." Warning: Washington, Main Street, none of us has "clean hands." We're all in bed with the "Happy Conspiracy," touched by greed, turning a blind eye to Wall Street's rapidly metastasizing moral and spiritual pathology: So ask yourself, do you believe America's widespread "lack of a moral compass" will eventually trigger another, bigger market and economic meltdown, pushing America into the next "Great Depression II?" |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 11:47 AM Response to Reply #35 |

| 37. Charitable Giving (BY GOLDMAN SACHS "DOING GOD'S WORK") |

|

http://epicureandealmaker.blogspot.com/2009/11/charitable-giving.html?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+blogspot%2Fepicureandealmaker+%28The+Epicurean+Dealmaker%29

In an otherwise less than sympathetic piece on the public relations travails of the Vampire Squid everybody loves to hate, Financial Times journalist Chrystia Freeland credits the investment bank's recently announced 10,000 Small Businesses initiative as "cleverly conceived" and "designed for maximum effect." I have to disagree. Like many of you, I am sure, I was impressed when I heard Goldman was going to donate $500 million to a myriad of small businesses, which are widely perceived to be the primary engines of job creation in our economy. Oh goody, I thought: half a billion bucks mainlined into the veins of those businesses best able to kick start the economy back into rude health. What a coup. Then I read the blasted thing. It is not pretty. Sixty percent of the committed funds will be distributed for "lending and philanthropic support," but this will be directed through "Community Development Financial Institutions." Call me a skeptic, but this does not sound like high powered money coursing directly into the working capital accounts of productive enterprises which can use it. Instead, it sounds like a $300 million slush fund for the functional equivalent of community NGOs. The remaining forty percent�200 million clams�will go toward "education." Oh great, Lloyd, that's just what every small businessman needs: an education. After all, everybody knows what the owner of a chain of dry cleaners or a machine tool factory really needs is "scholarships," greater "educational capacity," and mentoring by some half-assed social worker out of an abandoned storefront. Why stop there, though? Why not endow a hundred spots at Harvard Business School in perpetuity so Hmong immigrants can learn to apply CAPM and discounted cash flow analysis to their corner delicatessens? 1 Either that, or you could pull your head out of your ass and actually lend some money to these guys instead. Heck, set up a small business lender with half a billion in capital, lever it up ten to one, and loan five billion dollars out to struggling small businesses. You might actually spur some real economic growth, rather than employing an army of aspiring bureaucrats to fill out scholarship applications in triplicate. Plus, you might finally earn some respect from a country which suspects you and your peers are constitutionally incapable of taking a crap without consulting the Harvard Business Review or the McKinsey Handbook of Corporate Obfuscation for instructions. 2 This idea scales attractively, too: Put in a billion of equity, and loan out ten billion, and people might even stop whispering disparaging remarks about the size of your junk in the corridors of Capitol Hill. Now there's a return on capital. * * * On the other hand, given that you run an investment bank, if you want to raise some serious money for charity, you could always open a Swear Jar. Just make sure it's big enough. 1 Well, okay, that was a cheap shot. You and I both know doing any such thing would destroy the exclusivity and aura of an HBS education, which would be a societal catastrophe too terrible to contemplate. (Not to mention wasting two years out of the lives of otherwise productive elements of the economy.) Just kidding, bro. 2 I mean really, who comes up with this shit? I know you couldn't give a damn about tiny ass businesses which will never grow large enough to become paying customers of your firm, but you are theoretically announcing this program for public effect, no? Why not make it clear, simple, and understandable, instead of a convoluted, bureaucratic mess apparently derived from some EU functionary's wet dream? Bank? Lending? Ring a bell? |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 09:43 AM Response to Original message |

| 18. Plain Talk: Restore law and split up banks |

|

http://host.madison.com/ct/news/opinion/column/dave_zweifel/article_69ccafc6-42a4-50b2-8c23-a0903cb1e66c.html

Ten years ago, the Republican-controlled Congress � egged on by that champion deregulator, former Texas Sen. Phil Gramm � passed legislation that arguably did more to plunge the United States into our crippling great recession than anything else: It repealed the Great Depression era�s Glass-Steagall Act. Then on Nov. 12, 1999, an acquiescent Democratic president, Bill Clinton, signed the repeal into law. Glass-Steagall stood as a firewall between commercial banks and Wall Street since 1933, when the country�s leaders heeded the lessons of the 1929 stock market crash and set in place strict regulations in an attempt to prevent such an economic calamity from happening again. But the country�s financial institutions chafed for decades under Glass-Steagall�s restrictions. If only commercial banks could merge with investment banks and insurance companies, they argued, it would be so much better for the nation�s economy. Gramm, who infamously insisted that the U.S. had become a nation of whiners when the economy started to tank in the fall of 2008, fought for years to repeal Glass-Steagall and finally got his way. Get government out of the way of the free marketplace, he argued, ignoring the fact that historically conservative banks would be joining the high-risk investment community and all the pitfalls it represents. The repeal sanctioned the formation of the conglomerate Citigroup, for example, permitting commercial bank Citicorp�s merger with Travelers insurance corporation. Citigroup, which now included Citibank, Smith Barney, Primerica and Travelers, combined banking, securities and insurance services under one giant and, as we painfully learned, �too big to fail� financial institution. That�s how we got today�s Bank of America, JPMorgan Chase and the many other giants that participated in dicing and slicing subprime mortgages, and traded in complicated hedge funds, derivatives and other financial manipulations, which commercial banks were forbidden to do for more than 65 years. Now some of the biggies are coming to recognize the peril they and the country are in as a result. Last week, JPMorgan CEO James Dimon called the idea that any bank is too big to fail �ethically bankrupt� and added that regulators should have the power to let them fail. Even Citigroup�s co-founder, John Reed, said earlier this month that he�s sorry for creating the monster and that it was a big mistake when the bank merged with Travelers, opening the door to massive risk. Indeed, Reed said Glass-Steagall should be restored, joining former Federal Reserve Chairman Paul Volcker, who has been trying to convince the Obama administration of the need to return to the act�s strict regulation. That would mean breaking up the �too big to fail� institutions and restoring banks to being banks and investment houses to their own businesses. Breaking up the biggies would go a long way toward returning stability to the broken system, in which taxpayers are asked to save the conglomerates from their own bad behavior and then forced to sit by while the behemoths return to big profits and obscene bonuses. U.S. Sen. Bernie Sanders, the Vermont independent, has introduced legislation that would require the Treasury Department to identify the so-called �too big to fail� conglomerates and force them to break up within a year. Meanwhile, the Madison-based Center for Media and Democracy has started a new project called BanksterUSA to rally support for Sanders� legislation and advocate for prosecution of Wall Street executives who purposely manipulated markets for their private gain. Its motto is: �Too big to fail, but not too big for jail!� More information is on its website at www.BanksterUSA.org. After what we�ve gone through and what millions of innocent out-of-work Americans are still going through, it truly is time to restore Glass-Steagall and rid ourselves of these �too big to fail� conglomerates. Dave Zweifel is editor emeritus of The Capital Times. dzweifel@madison.com |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Thu Nov-26-09 09:46 AM Response to Original message |

| 19. David Freddoso: Your congressman's padded retirement plan |

|

http://www.washingtonexaminer.com/opinion/columns/Your-congressman_s-padded-retirement-plan-8551967-70368302.html