Health Insurers: Well Deny Coverage For Pre-Existing Conditions If Health Mandate Is Repealed

http://thinkprogress.org/health/2012/03/19/447157/health-insurers-well-deny-coverage-for-pre-existing-conditions-if-health-mandate-is-repealed/

Health insurers and supporters of the Obama administration’s health-care reform law are currently in the midst of drawing up possible contingency plans in case the Supreme Court overturns the Affordable Care Act’s individual mandate.

The insurance industry argues that premiums are likely to skyrocket without the individual mandate in place to aid in pushing millions of new enrollees into the marketplace, as healthy people will be less likely to buy insurance, while insurers will still be required to sell policies to all applicants. In fact, a repeal of the individual mandate would increase insurance premiums by 25 percent, according to a study released by the Robert Wood Johnson Foundation.

“The insurance reforms would have to change if the mandate were struck,” said Justine Handelman, vice president of legislative and regulatory policy for the Blue Cross and Blue Shield Association trade group.

Health-insurance officials say that if the mandate is repealed, “their first priority would be persuading members of Congress to repeal two of the law’s major insurance changes: a requirement to cover everyone regardless of his or her medical history, and limits on how much insurers can vary premiums based on age.” Their next step would be to “set rewards for people who purchase insurance voluntarily and sanction those who don’t.”

<more>

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

dewawi

(18 posts)Of course they are going to say this. How did Obama get the insurance companies to go along with his health care plan? He and they know they will make billions. What has been happening to insurance rates since Obama care was passed? they have gone up and up.

subterranean

(3,427 posts)Insurance companies will make billions. Rates will continue to go up and up. Which, by the way, they were doing since long before "Obama care" was passed.

Bill USA

(6,436 posts)( all emphases are my own_Bill USA)

Furthermore, the increase caused by the law is a result of the increased benefits it requires, a factor Republicans generally ignore. So far, insurance companies have been required to do the following:

■ Cover preventive care without copays or deductibles.

■ Allow adult children to stay on parents’ policies until age 26.

■ Increase annual coverage limits.

■ Cover children without regard for preexisting conditions.

~~

~~

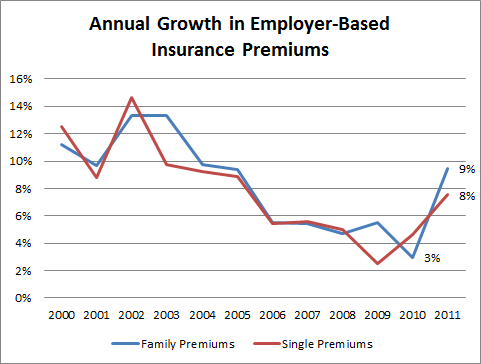

...experts we spoke with weren’t too surprised by this year’s findings. They point out that the 3 percent growth from 2009 to 2010 was unusually low. While it’s tough to discern a clear, long-term trend in the growth rates, the annual increase was holding steady at around 5 percent or 5.5 percent from 2007 to 2009. The growth rates had been at 10 percent and higher from 2000 to 2004. (See our chart below, which uses Kaiser’s employer survey numbers.) So, the 3 percent growth rate was “abnormally low,” says John Sheils, senior vice president of The Lewin Group, a subsidiary of UnitedHealth Group that operates independently of the health care company. He says it “would stand to reason that we’d get a boost” this year, possibly due to recovering losses or catching up on the cost of new equipment. A health policy analyst with the National Association of Insurance Commissioners agreed, saying that it was “not surprising to see it rebound like that.”

[center]

[/center]

[/center]

<more>

... the insurance companies went along with Obama's compromise approach because they knew without it they would be going out of business as a larger and larger segment of the population would not be able to afford health insurance which would have meant these people would have, out of necessity, been added to Medicare regardless of age.

julian09

(1,435 posts)wait til they take the mandate off, you'll see what going up really is, idiot.

He negotiated the mandate in return to get everyone insured, with preexisting conditions. Like insurance rates have not gone up before, mine didn't go up this year. Some people don't care if rates go up they use the emergency room.

BigDemVoter

(4,149 posts)And so many of these assholes who are all clamoring to overturn "Obama Care" would be the ones who would have their coverage DENIED.

Ron Obvious

(6,261 posts)Of course they do. Otherwise, without them being able to deny coverage for pre-existing condition, their customers would only get insurance when they get sick and drop it when they're well again. That'd be a completely unsustainable model of insurance. Every country that has an insurance model for medical care has a mandate. Of course, like e.g. Switzerland and the Netherlands, their rates are much more reasonable than ours. $150 a month gets you full coverage including vision and dental. My wife and I pay $600 a month for shitty coverage that pays for virtually nothing.

I'm afraid I suspected the worst when I heard Obama say during the campaign that his healthcare plan, unlike Hillary Clinton's, wouldn't have any mandates. That's the mark of a liar who'll say anything to get elected. He must have known better.

TheKentuckian

(25,023 posts)I am against this distortion that dictates we buy a for profit product at the discretion of our employers. We are fighting to have a government that can compel financial activity on post-tax income and further the conduit and selection of that activity be left to our shitty employers.

Worse, this power is not bounded. In fact, it MUST be argued that the power be unlimited in order to justify the pile of crap the insurance cartel has pushed and to no small degree written.

What freedom can a people have when a such a precedent is set? We can be made to do or not do literally anything if someone can argue that it has an impact on interstate commerce as virtually anything imaginable can.

Fascism isn't just a danger under such a legal framework, it is inherent.

Freedom isn't just limited under such a scheme, it is ended.

Bill USA

(6,436 posts)which keeps for profit insurers involved. But, it would have been impossible to go to a single payer approach and tell health insurance firms that the business of health insurance was fini.

I'm assuming you prefer a single payer approach because you said:

"I am against this distortion that dictates we buy a for profit product at the discretion of our employers"

.... which perfectly describes the system we had without HCR where we were completely at the mercy of your employer as to who you would be getting insurance from... and of course, at the mercy of the insurers who deny coverage as soon as you get 'too' sick.

Then of course, with the system in place before HCR when the health insurance was too expensive to afford you just went without medical insurance. Oh boy! At the rate we were going, in about 10 years we would have been approaching 40% of the people not being able to afford health insurance, meaning they would be going to the hospital for medical care. And we, the taxpayers, would have been footing the bill (through Disproportionate Share Payments - payments to hospitals to cover the cost of providing care to people who couldn't pay for their care) as well as through higher premiums for those who still could afford private insurance), - for medical care rendered in the most expensive way it can be done.

The approach which keeps private insurers in the game means that if you don't want the private insurers to deny coverage on the basis of a pre-existing condition - the insurers can only do this if everybody be is in the pool.

TheKentuckian

(25,023 posts)But against a mandate that dictates we purchase a for profit product at the sole discretion of our employers. AKA, being made to purchase at the company store.

A mandate where we as individuals, regardless of employer or employment status, could go onto an exchange and at least select our own mandated plan could be acceptable to me.

What I was arguing for was more of ending the employer based system than single payer, though I do favor single payer.

The current "reform" as you pointed out is a life preserver for the insurance cartel and keeps the current system in place far longer than it could sustain it's self. Without the mandate and lots of government money the current mess was on a sure path to suicide. 40% without coverage would likely collapse the present and now extended self same system.

Regardless, there are several other effective systems around the globe other than single payer, some that even use private insurance and mandates that can take various forms and structures that we not only never considered and evaluated but worse now have most people stuck in very uncreative little boxes to where they can hardly imagine any nuance in how to structure even market based reform. We certainly could have a market based reform that is very similar to what came out but remove employers as the middle man/gatekeeper for access.

The company store factor is a severe distortion and to get there one has to make the commerce clause so absolute that we are closer to slaves than citizens and employees.

The present law was designed from the root to prevent single payer or any serious reform. We have built a house on a foundation of corruption and have spread the corruption by advancing an unlimited financial authority doctrine to pass a "reform" law that leaves every existing profit center and piece of a brutally failed system in place in exchange for a handful of pay for play features that will not impact most people, as much good they do for those that are helped.

Framing this particular version of a mandate as the only possibility other than Single Payer is simplistic, dishonest, ignorant, or a mix of them all.

An easy fix would be to open the exchanges to one and all rather than insisting employers be the access point. It is one thing to dictate my commerce, it is another to say I must spend my money as my employer elects. The precedent is unacceptably dangerous to me, you are supporting an unbounded power to compel commerce and worse taking about 85% of Americans from the ability to choose how the compelled dollars are spent.

It is because smart people refuse to admit this is not the only way to structure this, even within a private model that I am forced to believe many of those that support this mess are wilfully dishonest and/or acting as useful idiots for those who profit from and gain contol under both the present and coming systems.

Only by actually increasing the systemic entropy can one essentially leave almost every piece of the existing system in place and call it reform.

I also object to the everyone in the pool language when there is no such thing. There are hundreds of pools, each with thousands of mini pools. Market fragmentation was not even addressed, much less solved. The fragmentation places severe limits on the consumer advantage to everyone being in the system. Everyone in is mostly an effort to force people to make the cartel profitable no matter how little value their "product" is to them individually and the subsidies to make sure that after the individual is squeezed for every copper that their profits are unaffected.

Amend to a national pool with individual choice going hand in hand with individual responsibility and I could be an ally but as constructed we have fascism combined with an unlimited government with a duty to protect and insure profit for it's "private partners".

I think this paradigm is only embraced out of a great desperation to pass something called "healthcare reform", rather than on the merits, precedents set, and even how the bill will actually play out.

There is nothing to fix, any improvements will require scrapping this mess and starting again and by your own estimation we were at least a decade closer to the system and the predatory cartel collapsing than we are now. We'll have what we have for at least 20 years, by design.

Uncle Joe

(58,342 posts)to institute universal single payer coverage and get rid of the dysfunctional, and immoral for profit blood money insurance system.

Thanks for the thread, Bill USA.