| Latest | Greatest | Lobby | Journals | Search | Options | Help | Login |

|

|

|

This topic is archived. |

| Home » Discuss » Topic Forums » Economy |

|

| Celebration

|

Fri Feb-01-08 05:35 PM Original message |

| Aggregate Reserves of Monetary institutions |

| Printer Friendly | Permalink | | Top |

| Fovea

|

Fri Feb-01-08 05:43 PM Response to Original message |

| 1. I can hear the chainsaws in the distance |

| Printer Friendly | Permalink | | Top |

| papau

|

Fri Feb-01-08 06:00 PM Response to Original message |

| 2. I did not know of this Vermont blog - interesting writer - but she is a little over the top |

| Printer Friendly | Permalink | | Top |

| Celebration

|

Fri Feb-01-08 06:28 PM Response to Reply #2 |

| 3. I agree |

| Printer Friendly | Permalink | | Top |

| Warpy

|

Fri Feb-01-08 07:26 PM Response to Original message |

| 4. I've said with every stupid rate cut that they needed |

| Printer Friendly | Permalink | | Top |

| Celebration

|

Fri Feb-01-08 08:59 PM Response to Reply #4 |

| 5. repeat of 1990 |

| Printer Friendly | Permalink | | Top |

| AnneD

|

Sat Mar-08-08 01:02 PM Response to Reply #4 |

| 24. Warpy.... |

| Printer Friendly | Permalink | | Top |

| Warpy

|

Sat Mar-08-08 07:03 PM Response to Reply #24 |

| 26. The Chinese aren't stupid |

| Printer Friendly | Permalink | | Top |

| AnneD

|

Sun Mar-09-08 08:24 PM Response to Reply #26 |

| 27. I've been watching the farm distribution system.... |

| Printer Friendly | Permalink | | Top |

| CGowen

|

Fri Feb-01-08 09:07 PM Response to Original message |

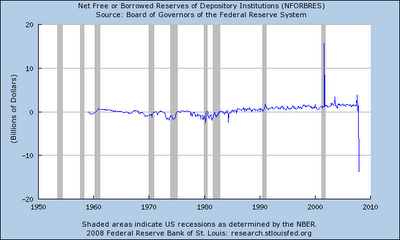

| 6. Could someone explain to me why the banks were so high in the positive around 911? |

| Printer Friendly | Permalink | | Top |

| Celebration

|

Fri Feb-01-08 10:14 PM Response to Reply #6 |

| 7. Not sure how the accounting works |

| Printer Friendly | Permalink | | Top |

| Celebration

|

Sun Feb-03-08 10:52 AM Response to Reply #6 |

| 8. changes |

| Printer Friendly | Permalink | | Top |

| CGowen

|

Sun Feb-03-08 11:11 AM Response to Reply #8 |

| 9. Discount rates were set higher to remove the stigma for banks, but |

| Printer Friendly | Permalink | | Top |

| Celebration

|

Sun Feb-03-08 11:34 AM Response to Reply #9 |

| 10. financial reporting sucks-BUT |

| Printer Friendly | Permalink | | Top |

| Celebration

|

Sun Feb-03-08 12:14 PM Response to Reply #10 |

| 11. So, my tin foil hat theory |

| Printer Friendly | Permalink | | Top |

| CGowen

|

Sun Feb-03-08 12:54 PM Response to Reply #11 |

| 12. I was reading something on hyperinflation, it's from wiki, I know, but nevertheless |

| Printer Friendly | Permalink | | Top |

| Celebration

|

Sun Feb-03-08 01:01 PM Response to Reply #12 |

| 13. Love Wiki |

| Printer Friendly | Permalink | | Top |

| CGowen

|

Sun Feb-03-08 02:31 PM Response to Reply #13 |

| 14. I think they changed it because they changed "Total Borrowing" |

| Printer Friendly | Permalink | | Top |

| Celebration

|

Sun Feb-03-08 03:01 PM Response to Reply #14 |

| 15. Aha |

| Printer Friendly | Permalink | | Top |

| CGowen

|

Sun Feb-03-08 07:20 PM Response to Reply #15 |

| 16. The Federal Reserve will conduct two auctions of 28-day credit through its (TAF) in February. |

| Printer Friendly | Permalink | | Top |

| Celebration

|

Sun Feb-03-08 10:49 PM Response to Reply #16 |

| 17. It is a bailout |

| Printer Friendly | Permalink | | Top |

| fasttense

|

Mon Feb-04-08 11:31 AM Response to Original message |

| 18. This is a very informative thread. |

| Printer Friendly | Permalink | | Top |

| Celebration

|

Mon Feb-04-08 12:45 PM Response to Reply #18 |

| 19. maybe they are taking their cues |

| Printer Friendly | Permalink | | Top |

| Celebration

|

Fri Mar-07-08 07:21 AM Response to Original message |

| 20. The Red Ink Increases |

| Printer Friendly | Permalink | | Top |

| CGowen

|

Sat Mar-08-08 11:17 AM Response to Reply #20 |

| 21. Solution: dump more money |

| Printer Friendly | Permalink | | Top |

| Celebration

|

Sat Mar-08-08 12:26 PM Response to Reply #21 |

| 23. What is the end game? |

| Printer Friendly | Permalink | | Top |

| CGowen

|

Sat Mar-08-08 06:40 PM Response to Reply #23 |

| 25. I don't know, but I heard the term "Endgame" before |

| Printer Friendly | Permalink | | Top |

| truedelphi

|

Mon Mar-10-08 12:05 PM Response to Reply #25 |

| 28. And remember, John Ashcroft tried to have both environmentalists and also |

| Printer Friendly | Permalink | | Top |

| Warpy

|

Sat Mar-08-08 11:22 AM Response to Original message |

| 22. I've been saying the same damned thing |

| Printer Friendly | Permalink | | Top |

| DU

AdBot (1000+ posts) |

Tue Apr 16th 2024, 03:15 PM Response to Original message |

| Advertisements [?] |

| Top |

| Home » Discuss » Topic Forums » Economy |

|

Powered by DCForum+ Version 1.1 Copyright 1997-2002 DCScripts.com

Software has been extensively modified by the DU administrators

Important Notices: By participating on this discussion board, visitors agree to abide by the rules outlined on our Rules page. Messages posted on the Democratic Underground Discussion Forums are the opinions of the individuals who post them, and do not necessarily represent the opinions of Democratic Underground, LLC.

Home | Discussion Forums | Journals | Store | Donate

About DU | Contact Us | Privacy Policy

Got a message for Democratic Underground? Click here to send us a message.

© 2001 - 2011 Democratic Underground, LLC