Welcome to DU!

The truly grassroots left-of-center political community where regular people, not algorithms, drive the discussions and set the standards.

Join the community:

Create a free account

Support DU (and get rid of ads!):

Become a Star Member

Latest Breaking News

General Discussion

The DU Lounge

All Forums

Issue Forums

Culture Forums

Alliance Forums

Region Forums

Support Forums

Help & Search

2016 Postmortem

Related: About this forumBig Banks that Donate Big $$$$ to Hillary Have Systematically Harmed PoC: RedLining, Etc:

Rampant Red-Lining Still Occurring:Biased Lending Evolves, and Blacks Face Trouble Getting Mortgages

NEWARK — The green welcome sign hangs in the front door of the downtown branch of Hudson City Savings Bank, New Jersey’s largest savings bank. But for years, federal regulators said, its executives did what they could to keep certain customers out.

They steered clear of black and Hispanic neighborhoods as they opened branches across New York and Connecticut, federal officials said. They focused on marketing mortgages in predominantly white sections of suburban New Jersey and Long Island, not here or in Bridgeport, Conn.

The results were stark. In 2014, Hudson approved 1,886 mortgages in the market that includes New Jersey and sections of New York and Connecticut, federal mortgage data show. Only 25 of those loans went to black borrowers.

Hudson, while denying wrongdoing, agreed last month to pay nearly $33 million to settle a lawsuit filed by the Consumer Financial Protection Bureau and the Justice Department. Federal officials said it was the largest settlement in the history of both departments for redlining, the practice in which banks choke off lending to minority communities.

Outlawed decades ago, redlining has re-emerged as a serious concern among regulators as banks have sharply retreated from providing home loans to African-Americans in the wake of the financial crisis.

Over just the past 12 months, federal, state and city officials have successfully required banks to expand minority lending programs and, in some instances, to pay penalties as part of redlining settlements in Buffalo; Milwaukee; Providence, R.I.; Rochester; and St. Louis. And more banks are facing scrutiny. The Justice Department now has more active redlining investigations underway than at any other time in the past seven years, officials said.

“Redlining is not a vestige of the past,” Vanita Gupta, the principal deputy assistant attorney general of the Justice Department’s civil rights division, said last month in a conference call with reporters.

Photo

Denis J. Salamone, chief executive of Hudson City Savings Bank, in 2008. Credit Brendan McDermid/Reuters

The effect on minority communities can be profound. Home ownership is a cornerstone of economic mobility, and without a stable group of homeowners, neighborhoods can be left vulnerable to blight and disrepair.

The recent cases illustrate how redlining has evolved. Bankers no longer talk openly about denying loans to black people. Instead, officials said, some banks have quietly institutionalized bias in their operations, deliberately placing branches, brokers and mortgage services outside minority communities, even as other banks find and serve borrowers in those neighborhoods.

snip

Fallout from the excesses of the subprime era in mortgage lending has, in some ways, set the stage for the discriminatory practices of today. As banks have tightened their credit lending standards to avoid risky loans, the percentage of blacks and Hispanics getting approved for mortgages has plunged.

snip

The issue is also achingly familiar. Until the 1960s, banks openly starved minority communities of home loans with the full backing of the federal government.

For decades, the Federal Housing Administration relied on so-called residential security maps to help decide which mortgages it would insure. The maps ranked and color-coded neighborhoods in cities across the country according to their perceived investment risk.

snip

Even after the passage of laws that banned discriminatory lending in the late 1960s and ’70s, redlining persisted. Its modern-day form, though, is far less overt.

New Jersey banks no longer respond explicitly, as some did in the late 1930s, when asked, “Are there any areas in which loans will not be made?” (“Newark,” some said.)

Most of Hudson’s customers would have had no idea that the bank was excluding blacks and Hispanics, officials said.

snip

Now the nation’s seventh-largest savings bank, it built its business on traditional mortgages and prided itself on its old-fashioned feel.

snip

https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=2&cad=rja&uact=8&ved=0ahUKEwj1t53F2-PLAhUQ92MKHYTHAKoQFggoMAE&url=http%3A%2F%2Fwww.nytimes.com%2F2015%2F10%2F31%2Fnyregion%2Fhudson-city-bank-settlement.html&usg=AFQjCNHthsIwBPckpD2nGOUYOdpAJYDHuQ

NEWARK — The green welcome sign hangs in the front door of the downtown branch of Hudson City Savings Bank, New Jersey’s largest savings bank. But for years, federal regulators said, its executives did what they could to keep certain customers out.

They steered clear of black and Hispanic neighborhoods as they opened branches across New York and Connecticut, federal officials said. They focused on marketing mortgages in predominantly white sections of suburban New Jersey and Long Island, not here or in Bridgeport, Conn.

The results were stark. In 2014, Hudson approved 1,886 mortgages in the market that includes New Jersey and sections of New York and Connecticut, federal mortgage data show. Only 25 of those loans went to black borrowers.

Hudson, while denying wrongdoing, agreed last month to pay nearly $33 million to settle a lawsuit filed by the Consumer Financial Protection Bureau and the Justice Department. Federal officials said it was the largest settlement in the history of both departments for redlining, the practice in which banks choke off lending to minority communities.

Outlawed decades ago, redlining has re-emerged as a serious concern among regulators as banks have sharply retreated from providing home loans to African-Americans in the wake of the financial crisis.

Over just the past 12 months, federal, state and city officials have successfully required banks to expand minority lending programs and, in some instances, to pay penalties as part of redlining settlements in Buffalo; Milwaukee; Providence, R.I.; Rochester; and St. Louis. And more banks are facing scrutiny. The Justice Department now has more active redlining investigations underway than at any other time in the past seven years, officials said.

“Redlining is not a vestige of the past,” Vanita Gupta, the principal deputy assistant attorney general of the Justice Department’s civil rights division, said last month in a conference call with reporters.

Photo

Denis J. Salamone, chief executive of Hudson City Savings Bank, in 2008. Credit Brendan McDermid/Reuters

The effect on minority communities can be profound. Home ownership is a cornerstone of economic mobility, and without a stable group of homeowners, neighborhoods can be left vulnerable to blight and disrepair.

The recent cases illustrate how redlining has evolved. Bankers no longer talk openly about denying loans to black people. Instead, officials said, some banks have quietly institutionalized bias in their operations, deliberately placing branches, brokers and mortgage services outside minority communities, even as other banks find and serve borrowers in those neighborhoods.

snip

Fallout from the excesses of the subprime era in mortgage lending has, in some ways, set the stage for the discriminatory practices of today. As banks have tightened their credit lending standards to avoid risky loans, the percentage of blacks and Hispanics getting approved for mortgages has plunged.

snip

The issue is also achingly familiar. Until the 1960s, banks openly starved minority communities of home loans with the full backing of the federal government.

For decades, the Federal Housing Administration relied on so-called residential security maps to help decide which mortgages it would insure. The maps ranked and color-coded neighborhoods in cities across the country according to their perceived investment risk.

snip

Even after the passage of laws that banned discriminatory lending in the late 1960s and ’70s, redlining persisted. Its modern-day form, though, is far less overt.

New Jersey banks no longer respond explicitly, as some did in the late 1930s, when asked, “Are there any areas in which loans will not be made?” (“Newark,” some said.)

Most of Hudson’s customers would have had no idea that the bank was excluding blacks and Hispanics, officials said.

snip

Now the nation’s seventh-largest savings bank, it built its business on traditional mortgages and prided itself on its old-fashioned feel.

snip

https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=2&cad=rja&uact=8&ved=0ahUKEwj1t53F2-PLAhUQ92MKHYTHAKoQFggoMAE&url=http%3A%2F%2Fwww.nytimes.com%2F2015%2F10%2F31%2Fnyregion%2Fhudson-city-bank-settlement.html&usg=AFQjCNHthsIwBPckpD2nGOUYOdpAJYDHuQ

The accused:

Last year, the city of Miami brought lawsuits against Wells Fargo, Bank of America, and Citigroup, alleging that the banks were steering black and Latino applicants towards high-interest, “predatory” loans.

A federal judge struck those lawsuits down, saying the city lacked standing. A federal appeals reversed that decision, though, on September 2, saying that banks could have foreseen the “attendant harm” that resulted from the predatory lending when they resulted in large numbers of foreclosures throughout the city.

Los Angeles filed lawsuits against four banks last year—J. P. Morgan, Bank of America, Wells Fargo, and Citigroup—accusing them of both traditional redlining (denying loans to people of color), and also the “reverse redlining” of making predatory loans rain on black and brown communities.

The city recently dropped the J. P. Morgan suit.

The suits against Bank of America and Wells Fargo are on appeal, while the Citigroup case goes to trial next year. The city says these banks have been engaging in these practices since 2004. Further up the coast, the city of Oakland has also sued Wells Fargo, accusing it of reverse redlining as well.

https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=5&cad=rja&uact=8&ved=0ahUKEwj1t53F2-PLAhUQ92MKHYTHAKoQFgg7MAQ&url=http%3A%2F%2Fwww.citylab.com%2Fhousing%2F2015%2F09%2Fredlining-is-alive-and-welland-evolving%2F407497%2F&usg=AFQjCNGc36olPBPIfr57OuOqmuEbRl2Whg

Last year, the city of Miami brought lawsuits against Wells Fargo, Bank of America, and Citigroup, alleging that the banks were steering black and Latino applicants towards high-interest, “predatory” loans.

A federal judge struck those lawsuits down, saying the city lacked standing. A federal appeals reversed that decision, though, on September 2, saying that banks could have foreseen the “attendant harm” that resulted from the predatory lending when they resulted in large numbers of foreclosures throughout the city.

Los Angeles filed lawsuits against four banks last year—J. P. Morgan, Bank of America, Wells Fargo, and Citigroup—accusing them of both traditional redlining (denying loans to people of color), and also the “reverse redlining” of making predatory loans rain on black and brown communities.

The city recently dropped the J. P. Morgan suit.

The suits against Bank of America and Wells Fargo are on appeal, while the Citigroup case goes to trial next year. The city says these banks have been engaging in these practices since 2004. Further up the coast, the city of Oakland has also sued Wells Fargo, accusing it of reverse redlining as well.

https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=5&cad=rja&uact=8&ved=0ahUKEwj1t53F2-PLAhUQ92MKHYTHAKoQFgg7MAQ&url=http%3A%2F%2Fwww.citylab.com%2Fhousing%2F2015%2F09%2Fredlining-is-alive-and-welland-evolving%2F407497%2F&usg=AFQjCNGc36olPBPIfr57OuOqmuEbRl2Whg

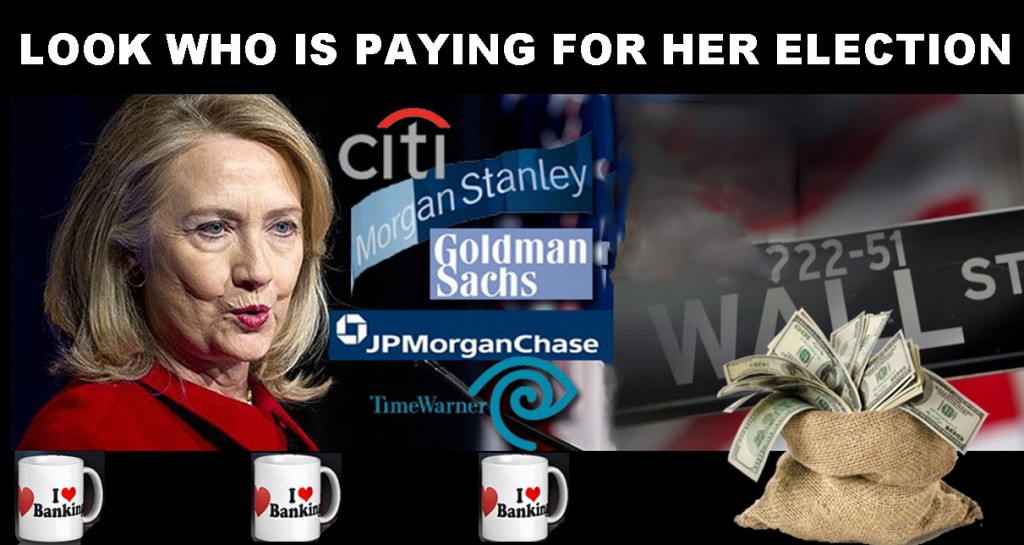

Clinton made $3.15 million in 2013 alone from speaking to firms like Morgan Stanley, Goldman Sachs, Deutsche Bank and UBS, according to the list her campaign released of her speaking fees.

"Her closeness with big banks on Wall Street is ....long-established and well known," former Maryland Governor Martin O'Malley has said on the campaign trail.

Sanders has been outspoken that the big banks are still "too big to fail" and should be broken up.

Clinton's anti-Wall Street policies stop far short of that, with proposals to tax short-term trading and impose a "risk fee" on big banks with assets over $50 billion.

Wall Street's reaction to her plan to regulation big banks was mostly a sigh of relief.

"We continue to believe Clinton would be one of the better candidates for financial firms," one analyst wrote.

Related: Wall Street isn't worried about Hillary Clinton's plan

?v=1429201091

?v=1429201091

http://money.cnn.com/2015/10/13/investing/hillary-clinton-wall-street/

"Her closeness with big banks on Wall Street is ....long-established and well known," former Maryland Governor Martin O'Malley has said on the campaign trail.

Sanders has been outspoken that the big banks are still "too big to fail" and should be broken up.

Clinton's anti-Wall Street policies stop far short of that, with proposals to tax short-term trading and impose a "risk fee" on big banks with assets over $50 billion.

Wall Street's reaction to her plan to regulation big banks was mostly a sigh of relief.

"We continue to believe Clinton would be one of the better candidates for financial firms," one analyst wrote.

Related: Wall Street isn't worried about Hillary Clinton's plan

?v=1429201091

to grasp the dangers that the Big Six banks (JPMorgan Chase, Citigroup, Bank of America, Wells Fargo, Goldman Sachs, and Morgan Stanley) presently pose to the financial stability of our nation and the world, you need to understand their history in Washington, starting with the Clinton years of the 1990s.

Alliances established then (not exclusively with Democrats, since bankers are bipartisan by nature) enabled these firms to become as politically powerful as they are today and to exert that power over an unprecedented amount of capital. Rest assured of one thing: their past and present CEOs will prove as critical in backing a Hillary Clinton presidency as they were in enabling her husband’s years in office.

http://www.commondreams.org/views/2015/05/07/clintons-and-their-banker-friends

Alliances established then (not exclusively with Democrats, since bankers are bipartisan by nature) enabled these firms to become as politically powerful as they are today and to exert that power over an unprecedented amount of capital. Rest assured of one thing: their past and present CEOs will prove as critical in backing a Hillary Clinton presidency as they were in enabling her husband’s years in office.

http://www.commondreams.org/views/2015/05/07/clintons-and-their-banker-friends

http://money.cnn.com/2015/10/13/investing/hillary-clinton-wall-street/

Hillary is veering from the truth when she suggests her $225,000 per speech fee, paid three times by Goldman Sachs, was “what they offered.”

It was not what they offered — it was what Team Hillary demanded.

A review of her 2014 tax return posted on her website shows that $225,000 was her minimum fee.

She received $225,000 for 34 of the 41 speeches listed on her tax return. Of the remaining 7 speeches, two were for 250,000 and the others for $265,000, $275,000, $285,000, $305,000 and $400,000. In total she received $9,680,000 for these speaking engagements in 2013.

Wall Street firms funded 14 of her 41 talks. In addition to Goldman Sachs, the list includes Morgan Stanley, Deutsche Bank, Fidelity Investments UBS and Bank of America. Her benefactors also include hedge funds and private equity firms like Apollo Management and Kohlberg, Kravis, Roberts.

Why did Hillary Take the Money?

Carl Bernstein, of Watergate fame and Hillary biographer, commented on CNN that the White House is “horrified that Clinton is blowing up her own campaign.” He said they can’t believe she took the money and didn’t see the ethical problems that would dog her.

It is not credible for her to argue that she took the money because she wasn’t sure she was going to run for president or that she was “dead broke.” She and Bill hauled in $139 million from 2007 to 2014.

http://www.huffingtonpost.com/les-leopold/hillary-not-truthful-abou_b_9185412.html

It was not what they offered — it was what Team Hillary demanded.

A review of her 2014 tax return posted on her website shows that $225,000 was her minimum fee.

She received $225,000 for 34 of the 41 speeches listed on her tax return. Of the remaining 7 speeches, two were for 250,000 and the others for $265,000, $275,000, $285,000, $305,000 and $400,000. In total she received $9,680,000 for these speaking engagements in 2013.

Wall Street firms funded 14 of her 41 talks. In addition to Goldman Sachs, the list includes Morgan Stanley, Deutsche Bank, Fidelity Investments UBS and Bank of America. Her benefactors also include hedge funds and private equity firms like Apollo Management and Kohlberg, Kravis, Roberts.

Why did Hillary Take the Money?

Carl Bernstein, of Watergate fame and Hillary biographer, commented on CNN that the White House is “horrified that Clinton is blowing up her own campaign.” He said they can’t believe she took the money and didn’t see the ethical problems that would dog her.

It is not credible for her to argue that she took the money because she wasn’t sure she was going to run for president or that she was “dead broke.” She and Bill hauled in $139 million from 2007 to 2014.

http://www.huffingtonpost.com/les-leopold/hillary-not-truthful-abou_b_9185412.html

Investment banks such as Morgan Stanley sought out high-risk loans disproportionately concentrated in non-white neighborhoods that were likely to default, bundled them and marketed them to investors, often, as the SEC complaint in the lawsuit settled with Goldman Sachs in 2010 illustrated, with the expectation that these loans would fail.

In doing so, they created a market for subprime loans and other high risk loans, driving a subprime industry that targeted minority borrowers and borrowers in largely non-white neighborhoods.

Goldman Sachs and Morgan Stanley are players in what is called the “secondary market” since they do not originate these loans, but they package them for investors through securitization. In many respects, it is the secondary market that set the terms for lending, not just to borrowers, but also for originating banks.

?itok=9P9Etjim

?itok=9P9Etjim

https://www.aclu.org/blog/civil-rights-today-landmark-case-adkins-et-al-v-morgan-stanley

In doing so, they created a market for subprime loans and other high risk loans, driving a subprime industry that targeted minority borrowers and borrowers in largely non-white neighborhoods.

Goldman Sachs and Morgan Stanley are players in what is called the “secondary market” since they do not originate these loans, but they package them for investors through securitization. In many respects, it is the secondary market that set the terms for lending, not just to borrowers, but also for originating banks.

?itok=9P9Etjim

https://www.aclu.org/blog/civil-rights-today-landmark-case-adkins-et-al-v-morgan-stanley

InfoView thread info, including edit history

TrashPut this thread in your Trash Can (My DU » Trash Can)

BookmarkAdd this thread to your Bookmarks (My DU » Bookmarks)

6 replies, 1164 views

ShareGet links to this post and/or share on social media

AlertAlert this post for a rule violation

PowersThere are no powers you can use on this post

EditCannot edit other people's posts

ReplyReply to this post

EditCannot edit other people's posts

Rec (18)

ReplyReply to this post

6 replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

Big Banks that Donate Big $$$$ to Hillary Have Systematically Harmed PoC: RedLining, Etc: (Original Post)

amborin

Mar 2016

OP

The Clinton Legacy Is Black Impoverishmentso Why Are We Still Voting for Hillary?

Octafish

Mar 2016

#3

GeorgiaPeanuts

(2,353 posts)1. K&R

valerief

(53,235 posts)2. Because

Octafish

(55,745 posts)3. The Clinton Legacy Is Black Impoverishmentso Why Are We Still Voting for Hillary?

From the crime bill to welfare reform, policies that Bill Clinton enacted—and Hillary Clinton supported—decimated black America.

BY: MICHELLE ALEXANDER

The Root, Posted: Feb. 10 2016

EXCERPT...

And it seems that we’re eager to get played. Again.

The love affair between black folks and the Clintons has been going on for a long time. It began back in 1992, when Bill Clinton was running for president. He threw on some shades and played the saxophone on The Arsenio Hall Show. It seems silly in retrospect, but many of us fell for that. At a time when a popular slogan was “It’s a black thing; you wouldn’t understand,” Bill seemed to get us. When Toni Morrison dubbed him our first black president, we nodded our heads. We had our boy in the White House. Or at least we thought we did.

Black voters have been remarkably loyal to the Clintons for more than 25 years. It’s true that we eventually lined up behind Barack Obama in 2008, but it’s a measure of the Clinton allure that Hillary led Obama among black voters until he started winning caucuses and primaries. Now Hillary is running again. This time she’s facing a democratic socialist who promises a political revolution that will bring universal health care, a living wage, an end to rampant Wall Street greed and the dismantling of the vast prison state—many of the same goals that Martin Luther King Jr. championed at the end of his life. Even so, black folks are sticking with the Clinton brand.

What have the Clintons done to earn such devotion? Did they take extreme political risks to defend the rights of African Americans? Did they courageously stand up to right-wing demagoguery about black communities? Did they help usher in a new era of hope and prosperity for neighborhoods devastated by deindustrialization, globalization and the disappearance of work?

No. Quite the opposite.

CONTINUED...

http://www.theroot.com/articles/politics/2016/02/the_clinton_legacy_decimated_black_america_so_why_are_we_still_voting_for.html

MisterP

(23,730 posts)4. politics is all about getting people to vote against themselves, to become so dependent

on pols to mediate and represent for them that they defend said pol no matter what they do: the voters have to be disciplined and groomed until all the facts in the OP are just ignored for "she can win" or "Republican lies"

Gwhittey

(1,377 posts)5. It does not help MSM

Has told so many lies.

amborin

(16,631 posts)6. kicking